blog

Pros and Cons of Using Clone Credit Cards in European Markets

Jun

Pros and Cons of Using Clone Credit Cards in European Markets

In recent years, clone credit cards have emerged as a notable trend within European markets, captivating the attention of both consumers and financial institutions alike. These financial tools, designed to replicate the functionality of traditional credit cards while offering unique advantages, come with their own set of benefits and challenges. As digital payment methods continue to evolve, it is essential to understand the pros and cons of using clone credit cards, especially in the context of a rapidly changing regulatory landscape and the ever-present threat of fraud. This article delves into the various aspects of clone credit cards, providing insights into their advantages, risks, and future implications for consumers and the financial industry in Europe.

Understanding Clone Credit Cards: Definition and Functionality

What are Clone Credit Cards?

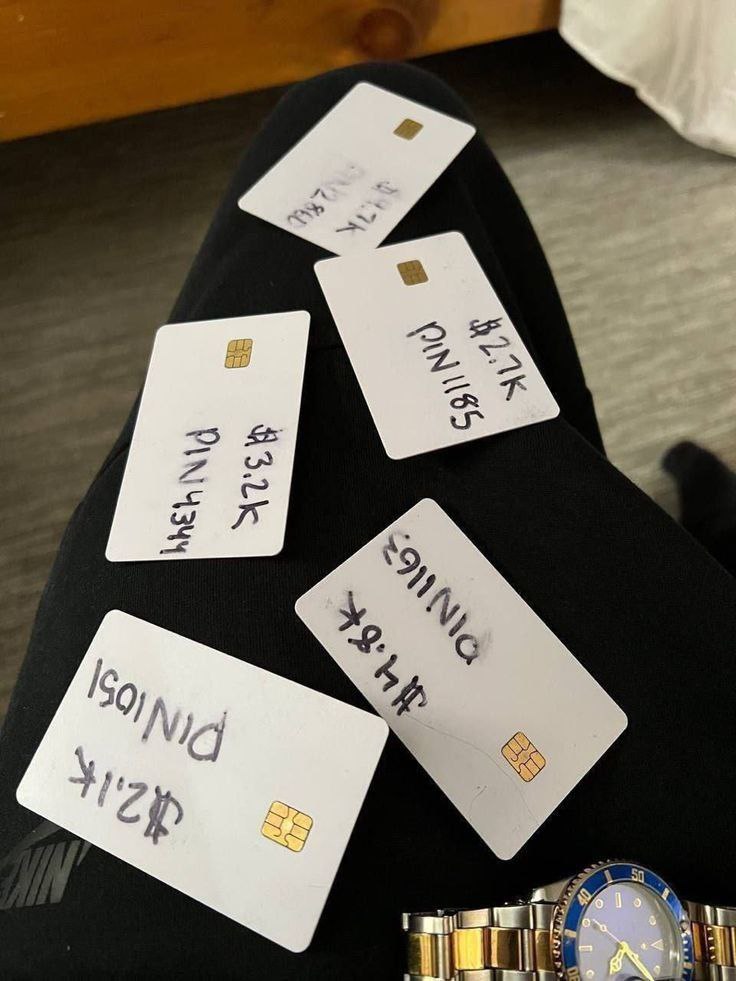

Clone credit cards are duplicated versions of legitimate credit cards, often used for fraudulent purposes. Think of them as the clone troopers of the payment world—similar in appearance but certainly not the same in intention. These cards often bear all the information of the original but are typically issued without the rightful owner’s consent, making them a hot commodity for cybercriminals.

How They Operate in the Market

In the murky waters of the dark web, clone credit cards can be bought and sold with alarming ease. Hackers obtain the information through data breaches, phishing scams, or even physical skimming devices placed on ATMs. Once they have this data, they create a duplicate card to exploit. Unfortunately, due to various regulations and sometimes lax enforcement, these cards can circulate in the market longer than you’d expect—leaving unsuspecting victims in their wake.

The Rise of Clone Credit Cards in European Markets

Market Trends and Adoption Rates

As the digital marketplace expands, so does the use of clone credit cards in Europe. Surprisingly, some studies have reported an uptick in the adoption rates of these cards among consumers who are unaware of the underlying risks. The charm of convenience sometimes overshadows the caution, leading to a steady uptick in usage—though the data varies by country and region.

Factors Driving Popularity

A combination of factors fuels the popularity of clone credit cards. Anonymity is a big draw for those wishing to keep their transactions under wraps, while others may be lured by enticing offers or limited-time deals that tempt them into making impulsive purchases with cloned cards. Plus, digital wallets and online shopping have made it easier for the less discerning user to stumble into the world of clone cards without realizing the potential pitfalls.

Advantages of Using Clone Credit Cards

Convenience and Accessibility

Clone credit cards can offer immediate access to funds, which might be tempting for users looking for a quick financial fix. No lengthy application process or waiting for a physical card to arrive in the mail—just grab a cloned version and start shopping! While this is a double-edged sword, it’s an undeniable perk for those who prioritize speed and convenience.

Enhanced Security Features

Ironically, some clone cards come equipped with advanced security features that make them look more legitimate. Chip technology or holograms on these cards can give users a false sense of security. Meanwhile, legitimate transactions can often be protected by different layers of verification, enticing users who think they’re protected from fraud—until, of course, they aren’t.

Potential for Budget Management

For some, using cloned cards can serve as a form of budget management—albeit a risky one. Because the transactions can be made in real-time, users might find it easier to track spending and manage their finances, assuming they aren’t facing the repercussions of a financial fraud investigation. But hey, if it works for you, why not?

Potential Risks and Drawbacks

Fraud and Identity Theft Concerns

Let’s get serious for a moment: the primary concern with clone credit cards is that they can lead to fraud and identity theft. One moment you’re enjoying a shopping spree, and the next, you’re dealing with your bank, disputing charges you didn’t make. The risk of becoming a victim is alarmingly high—it’s a waiting game nobody wants to play.

Impact on Credit Scores

Using clone cards can potentially derail your credit score faster than you can say “identity theft.” If unauthorized charges go unchecked, you could take a big hit when it comes to your credit history. It’s like trying to build a sandcastle at the beach only to have the tide wash it away—it’s a tedious process that can be easily undone by a rogue credit card.

Limited Consumer Protections

Unlike traditional credit cards, clone credit cards often come with limited consumer protections. Good luck trying to get your money back if you fall victim to a scam. Many card issuers are not liable for transactions made with cloned cards, leaving consumers high and dry. It’s like dancing with a shadow—you might look good, but in the end, you’re just left empty-handed.

Legal and Regulatory Considerations in Europe

Compliance with EU Regulations

Using clone credit cards in Europe is a bit like trying to smuggle a giraffe into a phone booth—it’s a tricky business, and the law is watching. The European Union has stringent regulations around payment services, primarily governed by the Payment Services Directive (PSD2). This aims to increase consumer protection and promote innovation while ensuring fair competition. If you’re considering the clone option, make sure you’re not stepping on legal toes. Just because you can, doesn’t mean you should (or that it’s legal).

Consumer Rights and Protections

In Europe, consumer rights are as cherished as a Sunday roast. Under EU law, consumers have robust protections against fraud and unauthorized transactions. If your clone credit card experience goes south, you might find recourse through your financial institution. However, it’s essential to remember that not all clone cards are created equal. The more reputable the provider, the more likely you’ll be covered under these consumer protections. So, if you do decide to dabble, make sure you know where you stand legally.

Comparing Clone Credit Cards to Traditional Payment Methods

Fees and Charges

When it comes to fees, clone credit cards can be like that friend who always “forgets” their wallet. They may seem appealing at first—often lower fees than traditional cards—but watch out for hidden costs. Some clone cards can come with transaction fees, currency conversion charges, or even monthly maintenance fees that can make your wallet feel much lighter. Traditional cards might have higher upfront costs, but the reliability could save you from unexpected surprises down the line.

Acceptance and Usability

Imagine strolling through a bustling European market, only to find that nobody accepts your clone card. Embarrassing, right? Acceptance can vary widely with clone credit cards. While some merchants might be on board, many still prefer the good ol’ traditional cards they’ve trusted for years. This can lead to frustration, especially when you’re trying to pay for that delicious gelato. Traditional payment methods are widely accepted, making them a safer bet for seamless shopping across Europe.

Best Practices for Safe Usage

Choosing Reputable Providers

When it comes to clone credit cards, think of it as dating; you wouldn’t want to swipe right on just anyone. Opt for reputable providers with a track record. Do your homework by checking reviews, verifying security measures, and ensuring they comply with EU regulations. A reputable provider will not only keep your information safe but also give you peace of mind, allowing you to focus on more important decisions, like whether you want a croissant or a pain au chocolat.

Monitoring Transactions Regularly

Keeping a close eye on your transactions is like regularly checking your fridge for expired food—nobody wants a nasty surprise. Make it a habit to monitor your clone card transactions regularly. Set up alerts for spending, review your statements, and report any suspicious activity immediately. This vigilance can help you catch fraud before it spirals out of control, and it might just save you from those awkward conversations with your bank.

Future Trends in Clone Credit Card Utilization in Europe

Technological Innovations

As technology continues to evolve at lightning speed, the world of payments isn’t left behind. Innovations like biometric authentication and digital wallets are training their sights on clone credit card alternatives. Expect to see more players entering the market, offering enhanced security features that make clone cards safer and more appealing. Soon, you might be paying with just a wink or a wave—just be careful not to scare your favorite cashier!

Conclusion

The romanticized image of cloned credit cards on European social media is a highly manufactured illusion. While the temporary “pros” of quick cash and luxury items look enticing in a 15-second video clip, they are heavily outweighed by the immediate, life-altering “cons.”

In European markets, where financial surveillance, AI-driven fraud detection, and international police cooperation are at an all-time high, the window for successfully using cloned data is incredibly small. The entities making real money are the dark web data-harvesters who face zero physical risk. The street-level buyers are simply operating as highly traceable fall guys. Ultimately, utilizing cloned cards isn’t a clever financial hack—it is a fast track to a European prison cell and a permanently ruined financial reputation.

Disclaimer

This article is strictly for educational, historical, and cyber-awareness purposes. The analysis of “pros and cons” is intended to illustrate the mechanics of financial crime and consumer vulnerability, not to promote or validate illegal activity. This website does not condone, facilitate, or encourage the purchase, creation, or use of cloned credit cards. Engaging in credit card fraud, identity theft, or electronic counterfeiting is a severe criminal offense punishable by heavy fines and lengthy imprisonment under European Union law and global jurisdictions.