blog

How Clone Cards Are Transforming the Payment Industry: Opportunities and Risks

May

The payment industry is undergoing a significant transformation, driven by technological advancements and evolving consumer preferences. Among the innovative solutions emerging in this landscape are clone cards, which offer both opportunities and challenges for users and businesses alike. While clone cards can enhance payment flexibility and streamline transactions, they also raise critical concerns regarding security and fraud. This article delves into the definition and functionality of clone cards, explores the emerging opportunities and inherent risks they present, examines the regulatory landscape, and considers best practices for safeguarding against potential threats. As the payment ecosystem continues to evolve, understanding the implications of clone cards is essential for navigating this dynamic industry.

Understanding Clone Cards: Definition and Functionality

What Are Clone Cards?

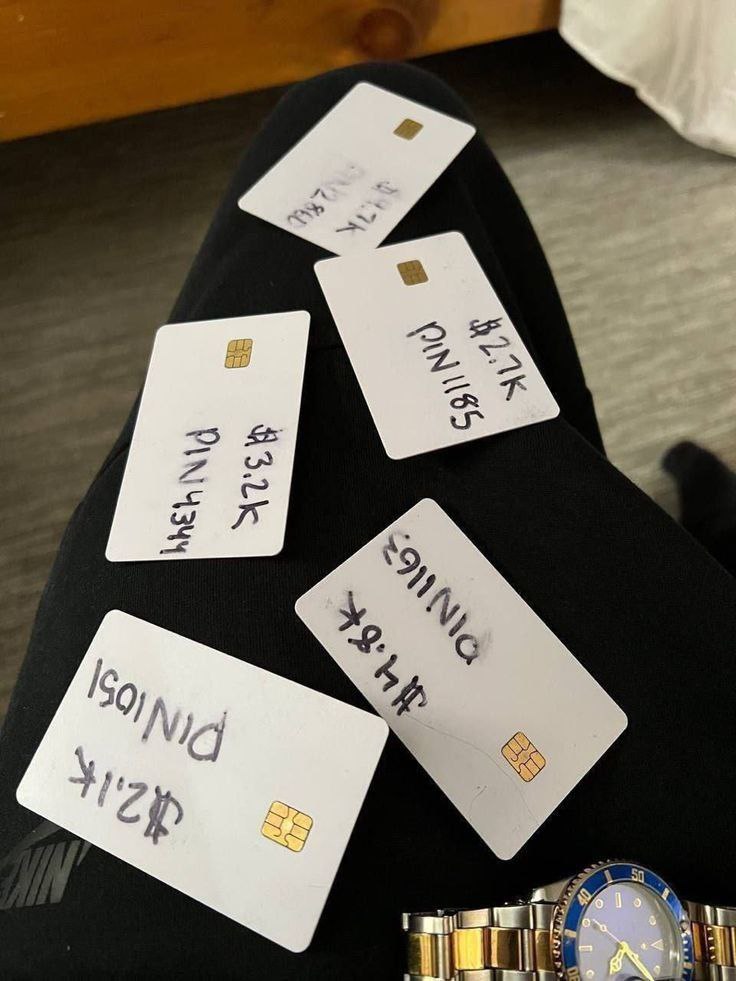

Clone cards are essentially digital replicas of existing credit or debit cards, created using technologies like card skimming or data breaches. Think of them as payment shape-shifters; they can mimic the details of a legitimate card, including the card number, expiration date, and security code, all while existing in the nebulous world of digital finance without your consent. Not just a wizardry trick, these cards can be used for online or in-person transactions, often leading to a cavalcade of headaches for cardholders and financial institutions alike.

How Clone Cards Function in Transactions

When a clone card is used, the process resembles any other card transaction from a superficial level—your purchase might go through and the merchant receives their funds, but behind the scenes, chaos reigns. These shuffled cards can undermine security measures like chip technology or EMV protocols. The cloned card sends the original card’s data without any of the physical security features, making it easier for fraudsters to score a fast buck while leaving the real cardholder to deal with the mess. Think of it as someone wearing a fake mustache attempting to sneak into a swanky event; it might work for a bit, but the ruse won’t last long before the truth comes out.

The Rise of Clone Cards in the Payment Ecosystem

Market Trends and Adoption Rates

Recent years have seen a curious uptick in clone card usage—almost like the unexpected popularity of pineapple on pizza. Market trends indicate that as online shopping explodes, so does the opportunity for cloning, with thieves continuously finding ingenious ways to exploit systemic vulnerabilities. Reports suggest that clone card transactions are rising, albeit in the shadows, as more individuals navigate the digital payment landscape. So while consumers might be opting for the convenience of contactless payments, others are banking on the lack of vigilance in security measures.

Technological Advances Driving Clone Card Usage

The very technologies designed to make our lives easier can sometimes feel like an open invitation to nefarious characters. Innovations in data analytics, machine learning, and even artificial intelligence have inadvertently paved the way for the proliferation of clone cards. Cybercriminals now have access to complex tools that allow them to siphon sensitive information at an alarming rate—from skimming devices at ATMs to malware lurking in untrustworthy apps. In this wild west of payments, technology is the double-edged sword; while it can enhance security, it can also equip fraudsters with sophisticated tools to create clone cards with impressive efficiency.

Opportunities Presented by Clone Cards

Enhanced Payment Flexibility for Consumers

While clone cards certainly have their dark side, they do present opportunities for flexibility in payment methods, much like having a trusty Swiss Army knife in your back pocket. Some legal and legitimate uses of derived card information might allow consumers to manage their finances more dynamically. This includes features like virtual cards that can easily be updated or discarded once they’ve served their purpose—an attractive option for online shopping enthusiasts who want to keep their primary card information under wraps.

Benefits for Merchants and Service Providers

For merchants, there’s a silver lining to the cloud of clone cards: an uptick in transaction versatility. Businesses can leverage card cloning technology, responsibly of course, to offer virtual or disposable cards for promotional offers or limited-time services. This fosters a sense of security and control for the customer, encouraging them to make purchases without relying solely on their main credit cards. In other words, clone card innovations can also enhance customer loyalty and create unique selling propositions in an oversaturated market.

Risks and Vulnerabilities Associated with Clone Cards

Fraud and Identity Theft Concerns

On the flip side, the surge in clone cards has raised significant alarms when it comes to fraud and identity theft. These cards can be exploited with alarming ease, leading to unauthorized transactions and a slow, painful recovery process for the victims. When a clone card waltzes into the scene, the original cardholder often faces the unfortunate reality of disputing charges while scrambling to secure their financial information. The ramifications stretch far beyond just a hacked account; they can affect credit scores, insurance rates, and even mental health as individuals grapple with the anxiety of fraud.

Impact on Consumer Trust and Brand Reputation

As cloned cards increase, so does the risk to consumer trust in brands and financial institutions. If you’ve been burned by fraud before, chances are you’re less likely to whip out your card with enthusiasm during checkout anytime soon. Businesses that fail to protect customer data may find themselves in hot water, facing negative reviews, bad press, and a rapidly diminishing customer base. After all, nobody wants to shop somewhere their personal information is treated like a piñata at a birthday party—swung at until it’s broken, with all the good stuff spilling out for criminals to enjoy.

Regulatory Responses to Clone Card Usage

Current Regulations Governing Clone Cards

The regulatory landscape surrounding clone cards is a bit like a game of whack-a-mole—just when you think you’ve got one problem solved, another pops up. Currently, laws vary widely across different countries and states. In the U.S., the Fair Credit Billing Act and the Electronic Fund Transfer Act provide some protections for consumers. However, regulations often lag behind technology, leaving gaps that savvy fraudsters are quick to exploit. Financial institutions are also required to adhere to compliance standards set by the Payment Card Industry Data Security Standard (PCI DSS), aimed at keeping card information safe. Yet, as clone cards and their related tech evolve, so too must the regulations designed to govern them.

Future Legislative Trends and Considerations

Looking ahead, we can expect a wave of new regulations aimed at tackling the complexities of clone cards. Policymakers are likely to focus on increasing accountability for financial institutions and pushing for more robust consumer protections. We may also see international cooperation, as cross-border fraud becomes increasingly common. Innovations like blockchain could inspire new legislative frameworks, promoting transparency and security in transactions. Ultimately, the challenge will be finding that fine line between fostering innovation and protecting consumers—like trying to balance on a seesaw with a weightlifter on the other end.

Future Trends: The Evolution of Payment Technologies

Emerging Technologies in Payment Systems

Payment technologies are evolving faster than a toddler racing for the cookie jar. From biometric authentication to contactless payments, new tools are making transactions quicker and more secure. Digital wallets and cryptocurrencies are also gaining traction, leading to novel payment experiences that could challenge the traditional plastic card model. Artificial intelligence is stepping in to help detect fraudulent activities in real-time, making it harder for clone cards to wreak havoc. As these technologies emerge, they’re not just changing how we pay—they’re reshaping our entire relationship with money.

Predictions for the Future of Clone Cards

As the payment landscape continues to shift, the future of clone cards is a mixed bag of possibilities. On one hand, advancements in security measures could make cloning less feasible, pushing fraudsters to find new, creative ways to exploit weaknesses. On the other hand, if regulations don’t keep pace with technological advancements, we could see an uptick in cloned cards as scammers strike while the iron is hot. The key will be a proactive approach from both industry leaders and regulators to stay one step ahead of the game—like trying to predict what your cat will do next (a true mystery, indeed).

Mitigating Risks: Best Practices for Consumers and Businesses

Security Measures for Consumers

Consumers can take several proactive steps to protect themselves from the perils of clone cards. First and foremost, regularly monitoring bank statements and credit reports is crucial; think of it as a financial health check-up. Utilizing unique passwords, enabling two-factor authentication, and setting up transaction alerts can also help ward off evil forces (a.k.a. fraudsters). Additionally, being cautious about sharing personal information and using secure payment methods—like chip-enabled cards—will act like a force field against would-be scammers. After all, it’s better to be safe than sorry, especially when it comes to your hard-earned dough.

Strategies for Businesses to Protect Against Fraud

For businesses, protecting against clone card fraud is more than a tech issue; it’s a holistic strategy. Investing in advanced fraud detection systems and training staff to recognize the signs of fraud can go a long way. Regular audits and compliance checks will help identify vulnerabilities. Implementing transaction limits and requiring additional verification for high-risk transactions can also mitigate risk—think of it as putting extra locks on your door. And let’s not forget the importance of fostering a culture of security awareness; employees should feel empowered to report suspicious activities. Together, these strategies create a safety net that helps keep businesses afloat in the sea of digital transactions.

Conclusion: Balancing Innovation with Security in Payments

Summarizing Key Takeaways

As we’ve navigated the tricky waters of clone cards, it’s clear that while they offer convenience, they also pose significant risks that both consumers and businesses need to navigate. Regulatory responses are evolving, but the balance between innovation and security is as delicate as a tightrope walker on a windy day. Emerging technologies like AI and blockchain hold promise for enhancing security, but they also require vigilant oversight to prevent new forms of fraud.